Make hay while the sun shines. Some observations on Australia’s domestic corporate airline market

- Peter Harbison

- Jul 23, 2025

- 3 min read

On 25-26 November at the ICC, Sydney, we’ll be holding Australia’s biggest ever corporate and business travel event. Here’s a glimpse at some of the subject matter.

Talk about global warming. It’s certainly time to be haymaking.

There’s a reason Qantas’ share price is up at record levels, about 50% higher than its peak just before the world changed, back in December 2019.

The reason is that one thing hasn’t changed in the domestic market since then: the number of seats being flown.

That’s to say, almost 6 years on, when historical growth would lead you to expect the domestic market to have grown by 15-20%, that ghostly demand is being squeezed into the same number of seats as back then.

With no prospect of additional competition now Rex has gone, there’s only one likely outcome. Up go the fares. Not too much, so as not to attract excessive attention, but enough to make investors salivate.

This is most apparent in the premium air travel market between Sydney and Melbourne – at least for Qantas.

Sydney-Melbourne is the world’s second busiest city pair, and the most lucrative, with a very high dose of corporate and business traffic.

After celebrating the new year by raising January business class fares by over 20% y-o-y, Qantas’ prices rose each month this year, according to Airline Metrics.

The June y-o-y increase was a more modest 10% or so, from an average $666 one way to $730. There’s no obvious reason for an increase, jet fuel prices aren’t up, although there is some upwards squeeze on salaries, but there it is.

That’s not the most interesting observation though – increases are to be expected, even if unwelcome. There’s more.

First is Virgin’s premium pricing behaviour has been different

Virgin with its 35% overall market share, is going after the mid-market, the “value” market. A bit opaque, but it doesn’t have a lot of wriggle room, sandwiched as it is between Qantas and Jetstar. The airline has no Chairman’s Lounge or other equally luxurious accommodation, nor does it have the enormous clout of the Qantas Loyalty programme, so the flying kangaroo has most of the big corporate market tied up.

That leaves Virgin’s business targets more focussed on SMEs.

Here, it seems, things may have been getting a bit tougher. After holding its y-o-y business class fares more or less steady up till March, they tumbled almost 20% y-o-y in May, then 10% in June, to a much more modest average $394 one way – not much more than half Qantas’ equivalent.

With an already massive gap in the Qantas-Virgin yield margins, it seems unusual at best to be moving to widen the premium gap further.

Perhaps Virgin has some information about small business that the Reserve Bank should be watching more closely. Or there are (probably) other things going on in this perversely obscure corporate market…

Qantas vs Virgin Australia - Business Fares on SYD-MEL: Jan-Jun 2025 and % change y-o-y

Source: Airline Metrics

* Note - Jetstar and Rex have been excluded from the Domestic average fare data

Secondly, Qantas’ economy fares have slid, while Virgin’s are rising

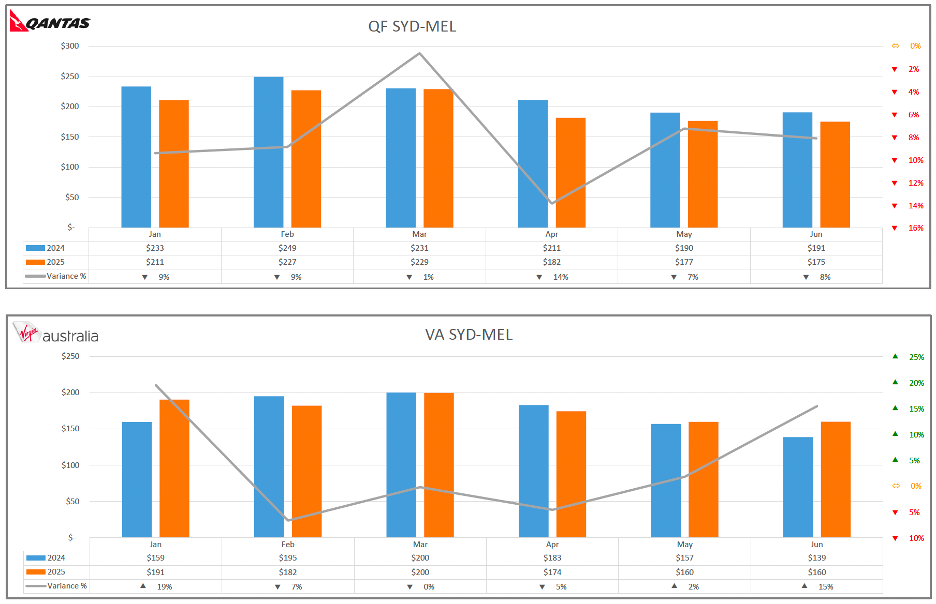

Even despite the capacity shortage, Qantas economy y-o-y fares on Sydney-Melbourne have however been heading south each month, to be down more than 6% for June, at $175 one way.

In contrast, Virgin’s have meandered around for the first five months, but then rose more than 10% y-o-y in June to $160.

These are of course average fares over the month, but the divergence is significant.

Interpreting revenue management strategies from these bare numbers is hazardous, but it would seem apparent that the lower yield market is softening – hardly surprising – though it doesn’t explain the divergent paths.

After floating off 30% of its equity in June, the good news for Virgin is that its shares too are riding relatively high, hovering around a 10% premium to the issue price.

So for the time being, everyone - on the supply side at least - is happy.

Qantas vs Virgin Australia - Economy Fares on SYD-MEL: Jan-Jun 2025 and % change y-o-y

Source: Airline Metrics

* Note - Jetstar and Rex have been excluded from the Domestic average fare data

These detailed data sets are supplied by Fare Metrics, a new service from Airline Metrics. The above description applies only to the Sydney-Melbourne route. Similar detailed fares data are available for other major Australian domestic routes.

The data are part of a new subscription-based monthly air fares report by Fare Metrics, designed to capture the evolving domestic and international market ahead of major NDC changes introduced by Qantas at the start of July 2025.

The data set captures ticketed edifact and NDC fares and provides a breakdown between Qantas and Virgin each month on major domestic city pairs. Click here for more information.

Comments